(12 min read – Published on 17th February 2020)

You must have noticed the launch of Disney+ and Apple TV+ lately. These two services are the new entrants in an unprecedented streaming war. In the USA alone, there are more than a dozen competing services. Netflix, Amazon Prime Video, Disney+, Hulu, Apple TV+, etc. But streaming is just the tip of the iceberg. What’s attracting most of the media attention. But there is a bigger moving force behind this battle. And it’s reshaping entire industries. Let’s take the razor blade market for instance. Created in 2011 and 2012, Dollar Shave Club and Harry’s started selling blades through online subscription services. Facing this menace, Gillette decided to counter-attack in 2016 with their own subscription: the Gillette Club. Shortly after, Unilever decided to enter the fight by purchasing Dollar Shave Club for $1Bn. While Schick tried to retaliate by purchasing Harry’s for $1.4Bn, before the Federal Trade Commission blocked the deal. Truth is, what’s happening in the streaming industry or the razor blade market is no coincidence. These are the symptoms of a bigger phenomenon. Threatening countless industries. From entertainment, to razor blades, retail, furniture, or even the tire industry. No one is immune from this danger. From this “gale of creative destruction”: the Direct-to-Consumer Revolution.

“The gale of creative destruction describes the process of industrial mutation that incessantly revolutionizes the economic structure from within, incessantly destroying the old one, incessantly creating a new one.” – Joseph Schumpeter, Capitalism, Socialism and Democracy.

What is Direct-to-Consumer?

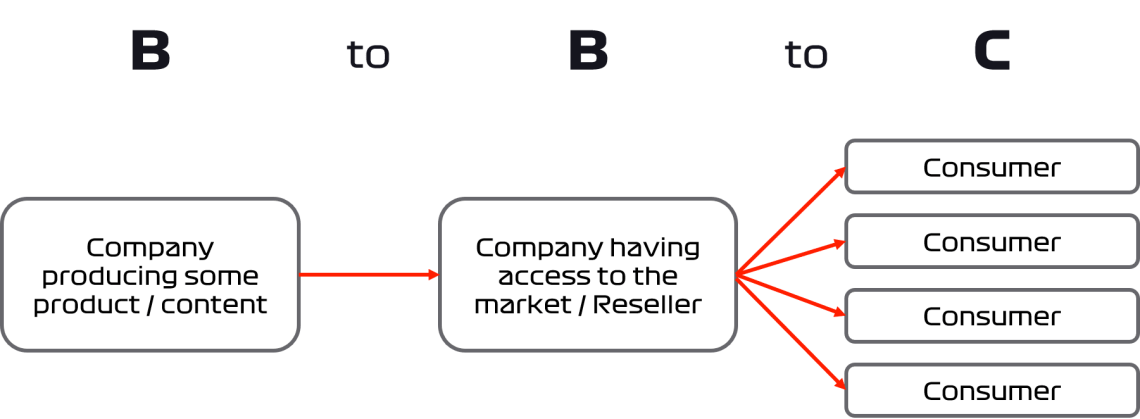

The Direct-to-Consumer (D2C) definition is simple. It means selling products directly to your end consumers. But most companies operate within a different environment: the B2B2C model (Business-to-Business-to-Consumer). This is when a company acts as a distributor for another company’s products. Sitting in between the manufacturer and the end consumer. Disney Studios is a good example. They produce movies, which are sold to different types of distributors. First to the movie theatre chains. Then, to the physical and digital distributors a few months later. Both selling the movie for a nominal fee. You can buy the DVD at your local store, or the online version on YouTube or iTunes. And a few years later, you can enjoy the movie on your TV through your traditional linear broadcaster.

B2B2C is the modus operandi for lots of industries. Nike primarily sells shoes through distributors such as Foot Locker. Gillette mainly sells razor blades through stores like Walmart. But the D2C Revolution occurs when the old B2B2C equilibrium is being threatened. When challengers start to reach the end consumers directly. There are three distinct case scenarios for this.

Scenario #1: Killing the middleman

The main reasons for a manufacturer to cut its middleman are simple: money and power. Going D2C improves your margins as your distributor is no more taking its share. And doing so gives you more control over the value chain of your product. But this is nothing new you might say. What’s new though is the rise of a new weapon of choice: digital. First, this weapon is cheap. Hosting an ecommerce website is very inexpensive and scalable thanks to AWS and the like. Second, this weapon is powerful. There’s never been as many online purchases and interactions before.

Digital makes the odds of a successful D2C attack very attractive. Back in the days, it wasn’t that easy to break even with a D2C offensive. Disney didn’t create their own brick-and-mortar movie theatre chain because it was just too expensive. The benefits would have never outweighed the costs. But the biggest reward of going D2C is the data. Collecting consumers data and connecting directly with them can unlock a wide range of opportunities. Disney clearly understood that when deciding to enter the D2C war with Disney+.

“The ability to have a direct relationship with the consumer gives us an opportunity to monetize much more effectively. […] We have a customer relationship through 3rd parties, and other than our theme parks, where we do have a direct relationship, we don’t know who these customers are. It is in knowing who they are that I think we have an opportunity that is extraordinary from a bottom-line perspective.” – Bob Iger, Disney’s CEO, CNBC interview in April 2019.

Scenario #2: Cutting the manufacturer

Any distributor would love to operate on a stand-alone basis. Cutting their manufacturer and producing their own product. Making them more independent and in control of their costs and margins. The tactical advantage of doing so relies in the distributor’s knowledge of the end consumers, and its ability to communicate directly with them. Walmart has been doing it for years. They have a long list of brands such as Sam’s Choice, Great Value, or Equate, which they push on the front shelf. Netflix is another good use case of this strategy. Once a DVD postal-based rental company, Netflix managed to pivot its business model. They became a subscription-based digital distributor for movies and series. They used to partner with media giants such as Disney (Marvel, Pixar, etc.), Comcast (NBC, DreamWorks, etc.), and WarnerMedia (HBO, Warner Bros, etc.). But now old allies have become enemies. Netflix is creating its own content called Netflix Originals. With successful series and films like House of Cards, Peaky Blinders, Bird Box and The Irishman. While at the same time their old allies are also entering the D2C war with their own streaming platforms. Disney with Disney+ launched in November 2019. Comcast with Peacock due to be launched in April 2020. And WarnerMedia with HBO Max planned for May 2020.

“The overarching strategy is that we’re continuing to drive toward our Original strategy. Over six years ago, we got into original programming betting that the license program would be more and more difficult to come by. […] And that has paid off. It’s very important for the business to continue pushing down that road.” – Ted Sarandos, Netflix’s Chief Content Officer in an earnings call in July 2019.

Scenario #3: The digital start-up invader

“By targeting a corporate giant’s weakness, a clever start-up with the right strategy, the right message and the right product value could create a new national brand virtually overnight. […] The DNVB revolution is one of the most dominant forces in the retailing business today.” – Lawrence Ingrassia, New York Times in January 2020.

Coined by Bonobos’s founder Andy Dunn in 2016, the term DNVB means Digitally Native Vertical Brand. It refers to start-ups breaking into B2B2C industries with a D2C approach. They challenge incumbent corporations by using digital channels directly, and by putting the consumers at the centre of everything they do. Over the past decade, many of these D2C invaders have become famous. Warby Parker (2010 – eyeglasses), Dollar Shave Club (2011 – razors), Glossier (2013 – beauty), Casper (2014 – mattress), or Soylent (2014 – nutrition). Until recently, the DNVB strategy was synonymous with success. With countless positive headlines in the news. But they have been heavily criticized since. It is very hard to keep attracting customers online past early adopters. The law of diminishing returns making each new online customer more expensive to acquire than the last. In order to succeed in their quest to dethrone B2B2C giants, DNVBs must truly be direct. By being too dependent on third parties to sustain their growth, DNVBs have lost their edge. Their growth heavily relies on a handful of digital platforms to capture new clients. Digital advertisers such as Facebook and Google. Or digital marketplaces like Amazon. In fact, Dollar Shave Club never generated any profit before being acquired by Unilever. Casper’s attempt at launching its IPO has been considered “a disaster”. While Brandless – once valued over $500m – just announced that they’re waving the white flag and closing their operations.

What’s the right strategy then?

“If I had an hour to solve a problem and my life depended on the solution, I would spend the first 55 minutes determining the proper question to ask… for once I know the proper question, I could solve the problem in less than five minutes.” – Albert Einstein.

Since every situation is different, it’s important to ask the right questions instead of applying ready-made solutions. There is no silver bullet answer to the D2C Revolution. And there is no one-size-fits-all plan. But there are a few key topics to address for any company potentially entrenched in, or facing a D2C conflict. Analysing the following three themes should help any company formalize their own strategy.

The product / The firepower

If you are on the manufacturer side, you must ask yourself one question. Do I have the right product for the D2C fight? For instance, Red Bull is producing a very successful product, its energy drink. But would that be enough to go direct-to-consumer? Probably not. Disney however made sure to increase their firepower before entering the D2C war. They expanded their portfolio with tactical acquisitions such as Fox, Lucasfilm, Marvel, and Pixar. Making their D2C offer very aggressive. The product you’re selling is very important if you are a distributor too. Not every product is easily replicable. And this might nip in the bud any potential chances of going direct-to-consumer. How easy would it be for a tire distributor to go D2C? They could leverage their network of point of sales. But chances are that producing tires by themselves might be just too hard. Not every distributor can easily plan a D2C expansion.

The competitors / The enemies

Keeping an eye on what your enemies are plotting is key. Not saying that you must mirror their strategy blindly. But if they opt for a D2C attack, they might have good reasons for it. But what’s more insidious than direct competitors are potential new entrants threatening your business model. Having DNVBs entering your B2B2C market is usually a sign that you might be missing out on a successful direct-to-consumer charge. Their usual tactic is to position their offensive with a subscription-based service, instead of just selling products directly to the end consumers. But not every B2B2C company is ready to disrupt their business model with such offer. Michelin – the 2nd largest tire manufacturer in the world – did exactly so. They launched in 2013 their D2C offer Tires-as-a-Service, targeting companies owning truck fleets. Instead of selling them tires, they chose to sell them mileage as a service. Nike also launched their own subscription offer in August 2019. Titled “Nike Adventure Club”, the service offers several kids’ pair of shoes per year to parents for a fixed monthly fee. But Nike isn’t the first to launch a subscription offer focused on kids. DNVBs such as Kidbox (2015) and Rocket of Awesome (2016) paved the way. While some retailers followed the subscription trend with their own service such as Urban Outfitters in May 2019.

The B2B2C partner / The “frenemy”

“Keep your friends close, and your enemies closer.” – Sun-Tzu, The Art of War.

Do not underestimate your allies. If you’re a distributor, the biggest D2C threat comes from your manufacturer. And the opposite is also true. It’s like a prisoner’s dilemma 2.0. Am I at risk of my partner cutting me out? Once disintermediated, a distributor loses its competitive edge. And by then, it might be too late to react. The balance of power between manufacturers and distributors is crucial. But not every manufacturer can afford to undercut their distributors. The distributor might have leverage, potentially threatening the manufacturer’s financial stability. And this is no surprise to only see giant corporations like Nike and Ikea cutting their ties with the biggest distributor in the world: Amazon. As the Seattle behemoth is now pushing more of its own private label brands on the platform. Jay Green from The Washington Post clearly explained how they operate in his article titled “Aggressive Amazon tactic pushes you to consider its own brand before you click buy”.

Taking the best of both worlds

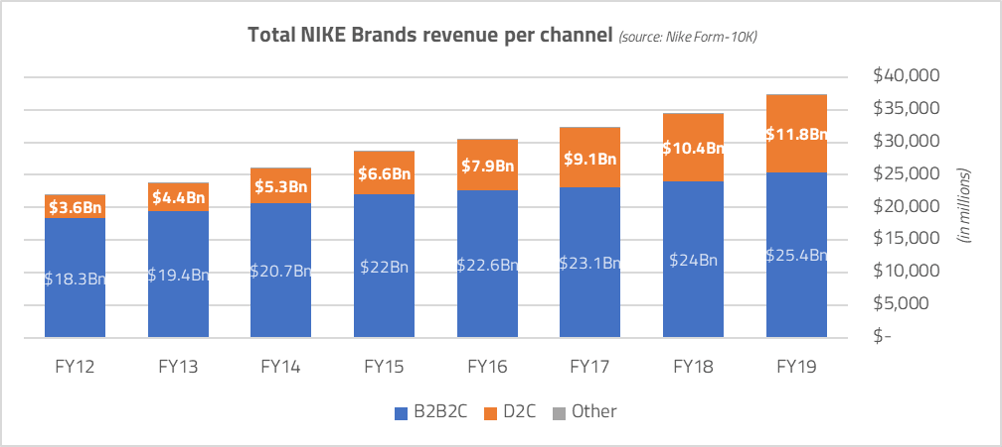

There is no perfect strategy to avoid the “gale of creative destruction” that the D2C Revolution is blowing. As every company and every industry is unique. But what’s interesting though is that some strategies look more successful than others. And one especially seems to be leading the pack. Instead of opposing D2C and B2B2C, some companies combine them. Taking the best of both worlds. And creating synergies along the way. Netflix and Amazon – both distributors at core – are embracing their D2C offers with Netflix Originals and Amazon private label brands. But they don’t plan on cutting their B2B2C activity any time soon. They want to maximize both D2C and B2B2C. Some manufacturers are also embracing the best of both worlds. Nike is a good example of that. Its D2C operation titled “NIKE Direct” – including owned retail stores and digital platforms – seems unstoppable. Nike’s D2C is growing 4x times faster than B2B2C over the past eight years, with a CAGR of +16.1%. And D2C now accounts for 32% of Nike’s total revenue.

This is no surprise as Nike heavily invested in their D2C operations. With acquisitions of analytics companies like Zodiac (March 2018) and Celect (April 2019). As referred in Nike’s press releases: “Zodiac’s acquisition strengthens the brand’s digital capabilities and accelerates its consumer direct offense strategy”, and “Celect is Nike’s latest acquisition fuelling its Consumer Direct Offense strategy, serving consumers personally at a global scale”. Nike even changed CEO to reflect this shift. They hired John Donahoe, e-commerce expert and former eBays President.

“I am delighted John will join our team. His expertise in digital commerce, technology, global strategy and leadership combined with his strong relationship with the brand, make him ideally suited to accelerate our digital transformation and to build on the positive impact of our Consumer Direct Offense.” – Mark Parker, Nike’s former CEO, in October 2019.

Applying the same mantra, some brands seem to be willing to go even further. Not only they have plans to go direct-to-consumer online, but they want to become distributors themselves. Ikea for instance looks to launch their own e-commerce platform that would include rival products. But as interesting this plan looks like, only time and execution will tell whether this is a success or not. Until then, we might even be witnessing another gale of “creative destruction”. Buckle your seat belt, and enjoy the ride!

—

Author’s note: This is a personal article. Any views or opinions represented in this article are personal and and do not represent those of people, institutions or organizations that the author may or may not be associated with in professional or personal capacity, unless explicitly stated.

Feature photo credit: Jason Hoffman / Thrillist